The National Debt Can Never Become Too Big: Hyperinflation

On flows versus stocks, government deficits versus government debt, and why "too much" federal borrowing will never lead to a hyperinflation crisis.

This is the second of three pieces on why the U.S. federal government’s debt will never become an economic problem, no matter how much it grows. The first piece is here.

We were discussing why the U.S. national debt can never become too big. [LINK]

The three possible scenarios you hear for how a debt crisis could unfold for the federal government are 1) private lenders will cut it off from borrowing anymore, 2) federal borrowing will drive up interest rates and choke off economic growth, or 3) federal borrowing will set off hyperinflation.

We dealt with the first scenario last time: The U.S. government can never actually run out of U.S. dollars, because it’s the only entity that’s legally empowered to create U.S. dollars. It has an infinite supply of them. So even if lenders did cut the federal government off, it wouldn’t matter, because it doesn’t actually need anyone to lend it dollars.

Regardless, lenders never will cut it off, because the federal agency that creates U.S. dollars—the U.S. Federal Reserve—uses that power to buy and sell U.S. Treasury bonds from the private markets. That’s how it conducts monetary policy and sets overall interest rates in the economy. Private markets will never stop buying Treasury bonds from the federal government because the federal government will never stop buying those bonds from them. The U.S. government is the main buyer of its own debt, with the private financial markets acting as a middle man between the Treasury Department and the Fed.

But let’s forget all that for a moment and just suppose private lenders did stop investing in U.S. debt.

At that point, people worry, the federal government would change the law so the Fed can just buy bonds directly from the Treasury Department—and thus cut out the middle man out entirely.

And they worry this could lead to hyperinflation. After all, if you can create an infinite supply of something, the danger isn’t that you’ll run out of it, but that you’ll wind up too much of it. And when it comes to U.S. dollars, “too many” means hyperinflation.

Here, for instance, is Noah Smith:

Every dollar that the Fed creates and gives to the government to spend is an extra dollar in the economy. If you printed a bunch of paper money and gave it out, eventually paper money would lose its value. The same is true of digital money. If you create bazillions and bazillions of dollars, eventually people will conclude that a dollar won’t be worth much.

Federal borrowing, according to Smith, is like an infinite corridor with an invisible pit. We don’t know how far down the corridor we can go before we fall in the pit. But eventually we’ll fall in.

Is Smith and everyone else who worries about this correct? Could too much federal borrowing lead to hyperinflation? That’s our subject this time.

The Concrete Mechanics of Inflation

Let’s start by laying out how inflation works. At the most basic mechanical level, inflation is driven by spending in the economy—“spending” here being just another word for “demand.” As we all know, prices rise when demand outpaces supply. That’s true of spending on individual goods and services, and it’s true of spending in the economy as a whole—i.e. “aggregate demand.”

Imagine the economy is a pipe. The size of the pipe, and thus how big a flow of water the pipe can handle, is determined by the economy’s overall physical capacity to produce goods and services. How many resources like steel, wood, minerals, concrete, and fuel does the economy have? How many office buildings and factories and electricity generators and chemical plants are operating? How many workers there are? And so on. Unlike a literal pipe, the size of the economic pipe grows over time, allowing it to handle a larger and larger flow of water. (At least, we hope it grows over time!) But at any given moment, the economic pipe can only handle so much.

The “water” in this analogy is, of course, spending. And inflation is when the flow of “water” through the pipe is too big for the pipe to handle. So the seams burst and the bolts blow out.

Here’s the thing: there’s a crucial distinction between the amount of spending in the economy and the amount of money in the economy.

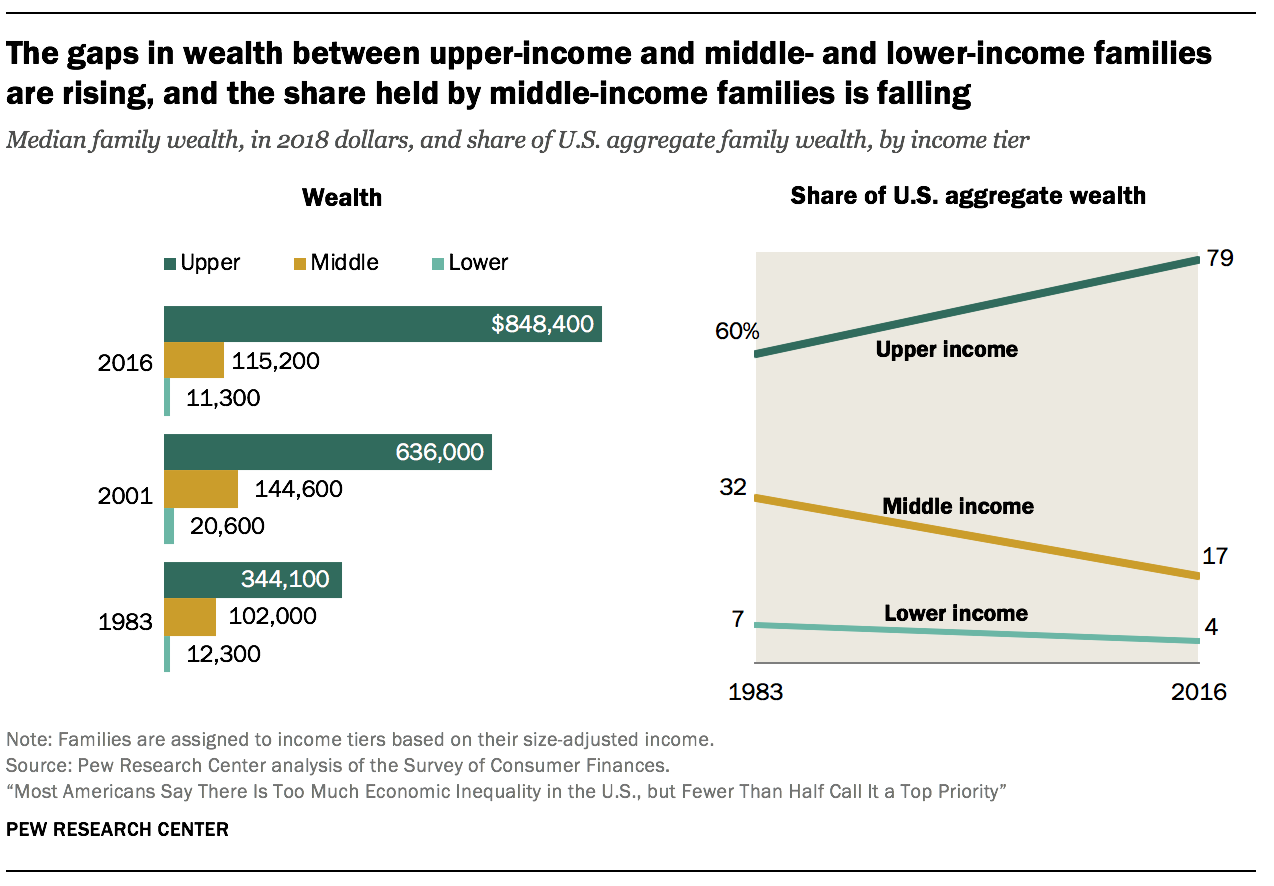

Because there’s always a ton of money in the economy that isn’t being spent. It’s called savings! Some of it’s sitting in bank accounts. Some of it’s invested in stocks and bonds and other financial assets. And a lot of it is invested in U.S. government debt—meaning U.S. Treasury bonds. (A very important point we’ll get back to.) All by themselves, Americans’ retirement savings totaled $37.8 trillion in 2023. Which is a ton of “potential” spending that hasn’t become actual spending. Actual spending in the economy was just over $27 trillion in 2023.

This all brings us to a crucial distinction to keep in mind: flows versus stocks.

Spending in the economy is a flow—a movement of a certain amount of units over a certain amount of time. Gross domestic product is also a flow. That’s why it’s measured annually, or quarterly, or whatever.

Savings, meanwhile, are a stock: an amount of money that just sits there. A stock can grow over time, but it doesn’t go anywhere.

Inflation is all about the flow.

At any given moment, the economy can only produce so many goods and services. If too much money flows through it too fast, there are no more people to hire, no more idle factories to start up, no more natural gas generators to turn on. You get the idea. Past that point, you’re just raising prices.

But our stock of savings isn’t being spent! It isn’t “flowing” anywhere. Ergo, there’s no physical limit on how big it can get. Savings are just electronic dollars in a computer somewhere. Or paper bills stuffed under a mattress. Or scribblings in a banker’s ledger, back in ye olden days. And all of those forms of saving can get as big as we want!

The Federal Deficit Versus the Federal Debt

Now we come to another crucial distinction: between the U.S. government’s budget deficit and the U.S. government’s debt.

The deficit is the gap between the federal government’s spending and its tax revenue—and thus, how much borrowing it did—measured over a given period of time. The debt is the sum total of all previous borrowing the federal government has done, and has not yet paid back.

The problem you often encounter is that everyone and their dog tends to talk about the deficit and the debt as if they’re interchangeable. Dylan Matthews did it in his piece on federal borrowing. Noah Smith did it too in the piece I mentioned at the beginning. He entitled it, “No one knows how much the government can borrow,” which suggests he’s worried about the size of the debt. Then he says this:

The government wants to borrow $100 trillion per day? The Fed can just credit their account with $100 trillion per day! This is why some people say the government has no borrowing constraint.

But borrowing $100 trillion per day is a measure of how much you’re deficit spending at a given moment. It’s not a measure of how much you’ve borrowed in total. So are we talking about a borrowing constraint or a deficit spending constraint?

This difference matters enormously, for two reasons.

First, when you reduce the budget deficit, the debt simply grows less fast. Even a tiny budget deficit will lead to a colossal debt if given enough time. To actually reduce the debt, spending must be cut or taxes must be raised (or both) so much that budget deficits reverse entirely and turn into budget surpluses. Then, to make any serious dent in the size of the debt, those surpluses must stay in place for a long time.

You need to be precise about whether you’re worried about the size of the deficit or the debt; reducing the latter is a much more radical proposition that reducing the former.

Second, as you probably noticed, the deficit is a flow, while the debt is a stock.

The deficit is how much money the federal government is spending into the economy, over and above how much money it’s taxing out. Per Smith’s example, deficit spending $100 trillion per day is a $100-trillion-per-day flow of spending into the economy. How that could cause inflation is pretty obvious: when combined with spending by private households and businesses, a big enough federal budget deficit could pump up the flow of money through the economic pipe so much that the seams burst.

So it’s perfectly reasonable to think the federal government has a deficit spending constraint.

But that’s distinct from a borrowing constraint.

Because the debt is a stock. It’s just a bunch of financial liabilities the federal government has built up. And those liabilities are financial assets for the rest of us—as mentioned, one of the main ways people save is by investing in U.S. Treasury bonds. You can quite literally think of the federal debt as a savings account the federal government runs for the benefit of the rest of the world; it gives American households and businesses, not to mention foreign governments and businesses, a place to store the excess U.S. dollars that they aren’t currently spending.

And by what possible mechanism could a stock of savings—which is, by definition, not being spent—affect inflation?

The Insidious Inflationary Threat of People Saving Too Much

Smith makes assumes that an increase in the supply of U.S. dollars inherently lowers the value of those dollars all by itself. In that first quote, he’s arguing that a big enough stock of U.S. dollars will eventually cause hyperinflation as a matter of mechanical inevitability.

But the price of something does not go down because supply goes up. It goes down because supply goes up relative to demand. The supply of U.S. dollars that decides the “price” of U.S. dollars in the economy is not how many dollars are out there in total.1 It’s how many dollars are being spent, as opposed to being saved.

Everything depends on how fast the money that you create—be it paper money or digital—enters the economy as spending. And on how many goods and services the economy can provide to absorb that spending. Money loses (or gains) its value relative to the total amount of supply the economy can create. And the pipe grows over time, remember?

This brings us back to the U.S. national debt. If it’s just everyone’s savings (and it is) then the only way it can cause hyperinflation—or even just inflation—is if it’s first turned into spending.

Of course, the bigger the U.S. national debt becomes, the more interest the federal government has to pay to private lenders. You could point to that as a form of spending that could drive inflation. Though that argument carries the amusing implication that when the U.S. Federal Reserve raises interest rates—and thus raises the federal government’s interest payments—it’s increasing, rather than decreasing, inflationary risk in the economy.

In practice, I don’t think that’s something we need to worry about. To get interest payments from the federal government, you have to own U.S. Treasury bonds. And if you’ve bought U.S. Treasury bonds, you’ve already got surplus dollars you want to save rather than spend. Which means you’ll probably just roll the interest payments on those bonds into further savings. Thus, whatever inflationary effect higher interest rates have in the economy is almost certainly completely overwhelmed by the deflationary effects.2

Anyway. The point is, to worry that the federal debt is “too big” is to worry that people’s savings are “too big.”

Specifically, you’re worried that all those savings will suddenly turn into spending. You’re worried that people will suddenly cash out all their U.S. Treasury bonds and then spend the money into the economy all at once. And the economy won’t have the capacity to handle it.

You can imagine scenarios that would drive people to do that. And we’ll get to them in a moment. But limiting the size of the federal debt as a hedge against the risk of hyperinflaton is just limiting how much people can save as a hedge against hyperinflation. You’re trying to keep everyone’s savings low enough such that, if they all did suddenly cash out their savings, it wouldn’t generate enough spending to send prices through the roof.

It’s basically: Hey everyone, some saving is fine. But let’s not save too much! Because, you know, we need to ward off the risk of hyperinflation.

And when you put it like that, it’s a kind of obviously insane.

Hyperinflation Isn’t That Mysterious

But why would everyone in the U.S. economy suddenly spend so much all at once? Hyperinflations do happen. What actually makes them happen?

Noah Smith’s answer is that we really don’t know; the ways of hyperinflation remain mysterious to the economics profession. He’d like to see a lot more study and research done on the question.

I certainly don’t object to more study and research. But with all due respect to the economics profession, I don’t think hyperinflation is particularly hard to understand.

Take smartphones: they’re both quite expensive and in high demand. Yet their price does not go up and up and up. Everyone’s desire for smartphones, their desire to save, and how much money they have to spend, are all forces that have reached a stable equilibrium.

If some disaster—a tsunami, a terrorist attack, whatever—destroyed all but one of the smartphone factories, then their price would definitely jump way up. But it wouldn’t go up forever. A lot of people would look at the new price tag and decide they can live without a smartphone. The market would reach a new equilibrium at a higher price, reflecting the new lack of supply.

Indeed, producing that sort of equilibrium is the whole point of a well-functioning market economy! And eventually, smartphones would become cheaper again, as the higher price incentivized re-investment in smartphone production. Huzzah, markets!

Now imagine that same scenario playing out with something like food, or gas. Supply suddenly becomes way more scarce, and the price jumps way up. Do a lot of consumers suddenly decide they can just do without food or gas? That they can just wait however long it takes (Months? Years?) for price signals and market incentives to drive investment and rebuild the food or gas supply chain?

I doubt it.

In that case, you can imagine the price just going up and up and up endlessly, as people desperately cash out their savings to buy whatever food or gas is available. And just never give up.3 That’s when a hyperinflationary spiral starts to look like a real possibility.

Here’s what I would suggest: Inflation is just a bidding war over scarce resources. And the bidding war ends in one of three ways. One, supply recovers so the resource is no longer scarce. Two, people decide that having the resource isn’t worth the grief and they stop bidding on it. Or three, they just run out of money with which to bid.

Hyperinflation happens when all three mechanisms fail to kick in.

For whatever reason, something physical has happened in the real world that prevents supply from recovering—or at least prevents it from recovering with anything like the necessary speed. Next, it has to be a resource that people just can’t do without, like food or energy.4 And third, money has to be flowing into the economy from some source, such that people just never run out of the spending needed to keep the bidding war going.

Hyperinflation As a Pitfall For Underdeveloped Economies

That third criteria—people just never running out of money—is where you can see a role for the federal debt. If that debt is just peoples’ savings, then the bigger it is, the more savings they’ll have to burn through before they run out of money.

But like I said, limiting how much people save in order to avoid this scenario is rather like starving people to prevent them from developing bulimia.

More often, what you see happen is that a government responds to this kind of crisis by just creating more and more money that does immediately get spent. Not surprisingly, given what we’ve covered thus far, the source of the infinite spending in a hyperinflationary crisis is government deficits, not government debt.

For one thing, hyperinflations almost always happen in countries that are still economically developing. So they haven’t yet built the domestic capacity to produce certain key needs that people can’t do without—food, energy, medicine, et cetera. So the country has to rely on imports. Often, in order to afford those imports, the country gets stuck supplying one key export to the rest of the world, like oil or cheap manufactured goods.

Then something goes terribly wrong, and what domestic production capacity the country has breaks down. If it’s supplying a key export, it can’t supply it anymore. Or its borrowed a ton of foreign currency (as opposed to its own currency) to buy those imports. And now it can’t pay those loans back. Or, most likely, some combination thereof. The upshot is the country suddenly needs a bunch of key goods which it can’t produce itself, and which it can no longer afford to import. So the domestic price of those goods goes through the roof.

Unfortunately, economically developing countries are also more likely to be ruled by incompetent dictators and autocrats. Indeed, terrible policies and economic mismanagement by said dictators and autocrats is often why the country gets into this sort of impasse in the first place.5 And once the crisis hits, rather than fix the physical breakdown in the economy’s ability to generate supply, the country’s government just prints lots of its own currency, and gives it to people so they can afford the higher prices.

But that doesn’t make the imports any more affordable in the foreign currency they’re actually purchased in. It just drives the imports’ price in the domestic currency higher and higher.

Hence, hyperinflation.

If you look at examples of hyperinflations around the world, I think you see some version of this play out again and again. Thanks to government mismanagement or some other event, there’s a catastrophic breakdown in the economy’s physical capacity to produce key things that people really can’t do without. That sets off a socially and politically brutal bidding war. And then the government responds, not by fixing the problem, but by just creating more money for people to spend in the bidding war.

But that’s all a matter of two much deficit spending too fast; not a matter of too much debt.

Hyperinflation As a Hazard of War

One takeaway here is that it’s just really, really difficult to imagine hyperinflation occurring in a prosperous, advanced, diversified economy like the United States. We’re not especially reliant on imports. Our domestic productive ability to meet our own needs is sophisticated and vast. It would take a lot of work to destroy all that.

In fact, on the very rare occasions when you do see an advanced economy plunge into hyperinflation, it’s the result of war—think Germany after World War I.

For one thing, in war, the enemy often literally destroys your economy’s physical capacity to produce stuff. But even if that doesn’t happen, war commandeers your economy in extremely unproductive ways. During peacetime, pretty much all the goods and services we make renew our capacity to produce in the future in some way. Investment obviously does this. But even most forms of consumption—food, shelter, medicine—do as well. The line between “investment” and “consumption” is actually pretty fuzzy. But war involves a lot genuinely unproductive economic activity.

You wind up devoting tons of resources to building bullets and tanks and bombs and planes that all get sent to the front and blown up. And that’s it. From a technical economic perspective, it’s all quite pointless. Meanwhile, you’re trying to keep your population going with whatever production capacity hasn’t been commandeered by the war effort. And even as you’re reducing your economy’s ability to meet everyone’s needs, you’re spending tons of money to finance the war effort.

Thus, the policies of warmaking are a recipe for inflation in a way most other government policies just aren’t.

I quipped last time that it’s hard to imagine anything short of nuclear war or a zombie apocalypse or a Hugo Chavez-style dictatorship destroying the value of U.S. Treasury bonds. Of course, a hyperinflation crisis would certainly do the trick. But that’s kind of tautological. Because it’s hard to imagine anything short of nuclear war or a zombie apocalypse or a Hugo Chavez-style dictatorship setting off a hyperinflation crisis in the U.S. dollar.

In fact, I’m not even totally sure Noah Smith’s hypothetical $100-trillion-per-day budget deficits would set off hyperinflation! A lot depends on what the government is spending that money on. If it’s employing people and buying resources directly, then yes, deficits like that would be hyperinflationary. But if it’s just giving the money to people to spend via welfare programs, it might all just get socked away into savings!6

If the first two criteria to prevent inflation are already in place—if our economy is prosperous and able to meet everyone’s needs, and the physical capacity is there to reach market equilibrium—then simply having infinite spending available to the public might not matter. I’m honestly not sure. But I think it’s a possibility you have to take seriously.

At the same time, I don’t think we need to try this out and see what happens. If anyone wants to argue that we shouldn’t deficit spend $100 trillion-per-day because it risks hyperinflation, I’d say that’s a totally reasonable concern!

What isn’t reasonable is worrying that a federal debt of $100 trillion will set off hyperinflation. Or $500 trillion. Or $100 quadrillion. Or a bazillion bazillion. Because the mechanism simply isn’t there. “Too many” people socking “too many” U.S. dollars away in U.S. Treasury bonds instead of spending them definitely isn’t going to drive prices through the roof.

Wherever a hyperinflation crisis does come from, it will not come from the size of the U.S. national debt.

I think you could argue that the raw supply of U.S. dollars, saved or spent, can change the value of U.S. dollars relative to other currencies. But that’s only a problem if you don’t supply the world’s premiere reserve currency and if you’ve got an underdeveloped economy that’s heavily dependent on imports for key economic needs.

Even more so because the distribution of wealth ownership—including ownership of U.S. Treasury bonds—is wildly unequal. The people and institutions getting the majority of federal government interest payments already have plenty of money. They don’t need those interest payments to give them the ability to spend more. If ownership of U.S. debt was evenly distributed, then federal interest payments would effectively be a universal basic income—which might be more inflationary. But we’re nowhere close to that world. Meanwhile, the vast majority of regular Americans who do own U.S. Treasury bonds own them as a part of a retirement savings portfolio.

{kind=link}

Supply crunches in gas or other forms of energy can be particularly nasty for yet another reason: energy is an input into pretty much all other economic activity. If energy becomes scarcer and pricier, then everything becomes scarcer and pricier.

Admittedly, the line between what people can and can’t do without is fuzzy, and involves some degree of squishy social relations. Smartphones used to not exist. So obviously we didn’t need them then. But if the supply of smart phones suddenly dried up today, we’d get a massive disruption in how human beings communicate and coordinate with each other. And we’d need to relearn a lot of old ways of doing things. But I imagine we’d figure it out. So I’d say smartphones are more necessary than video game consoles or a high-tech coffee makers. But probably still way less necessary than food and energy and medicine and so forth. Anyway, the point is, the divide between things we can do without and things we can’t is fuzzy and hard to pin down. But it is there. Human demand is not actually infinite. That’s why we can have savings even as markets reach equilibrium in the first place.

If you are so inclined, you can look at “terrible policy and economic mismanagement by said dictators and autocrats” and cry “Socialism!” But as Noah Smith rightly noted in his portrait of how the Chavez and Maduro regimes wrecked Venezuela, there are lots of countries that run some version of “socialist” economic policy, or where some key industries are public owned and managed. And they do fine! No hyperinflation crises. Regardless of the grand “framework” your economy is organized around—capitalism, socialism, whatever—there’s no substitute for competent technocratic policymaking.

I’m sure a lot of prices would jump at first: We’re a pretty unequal country, so a lot of people would suddenly find themselves with money to spend to raise their living standards. And their labor would become a lot more expensive. (And those changes would all be, you know, good!) But eventually our market economy would presumably sort things out, reach a new equilibrium, and all that excess government spending would go into everyone’s pockets and from there into savings.